Dairy Market Update, October 2011

Print

Print Email

EmailDairy market fundamentals suggest a great deal of risk remains in the market.

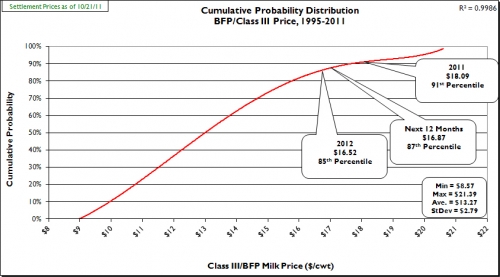

Prices: On Friday, October 21, 2011 spot prices for cheddar cheese blocks and barrels at the Chicago Mercantile Exchange (CME) were $1.7200/lb and $1.6900/lb, respectively. CME block and barrel cheese prices are up slightly since late September (9/28/11), +$0.0025/lb and +$0.0450/lb, respectively. During the same time period, butter is up (+$0.1000/lb) to $1.8600/lb. CME Class III futures averages (10/21/11) for 2011 were up (+$0.1841/cwt) to $18.09, while the next 12 months and 2012 averages were down to $16.87/cwt (-$0.0150/cwt) and $16.52/cwt (-$0.2575/cwt), respectively. These Class III futures averages correspond to potential USDA Michigan mailbox prices for 2011, the next 12 months, and 2012 of $19.08/cwt, $17.86/cwt, and $17.51/cwt, respectively. Figure 1 is a cumulative probability distribution of all USDA BFP/Class III monthly prices from 1995-present. The figure shows the current (10/21/11) CME Class III futures averages for 2011, the next 12 months, and 2012 are at the 91st, 87th, and 85th percentiles, respectively.

Figure 1: Cumulative probability graph of USDA announced monthly BFP/Class III prices (1995-present) and current CME futures averages.

Supply: In September U.S. milk production increased above trend (+1.6%, 1995-2011) at +1.7% compared to September 2010. September was the second consecutive month milk production grew above trend increase. September production in Michigan increased +1.9% compared to September 2010. The size of the U.S. dairy herd remained constant from August to September, but is up 88,000 head versus September 2010. Dairy cow slaughter numbers in 2011 continue to run well ahead of last year, up 89,900 head compared to last year (through 10/01/11). Average U.S. cull cow prices remained high in September at $69.70/cwt (+26.3% compared to September 2010). Milk production per cow for January through September was below trend increase (+0.7%); however, it rebounded nicely from the July heat-induced decline. The USDA reported an increase in dairy feed prices in September of 58.4% compared to September 2010. September’s income over feed costs were down 1.4% (-$0.11/cwt) as compared with September 2010.

Demand: The USDA reports total commercial disappearance in 2010 increased 3.3% over 2009, well above the 1995-2009 average increase (+1.6%). All categories of wholesale dairy products showed above trend increases in disappearance for 2010 except fluid milk products. Total commercial disappearance for 2011 has weakened and is below trend increase (+1.3%) through July. All-time monthly records were set for January, February, March and April, but May, June and July were down 1.4%, 3.2% and 0.2%, respectively, as compared with May, June and July 2010. Through July, disappearance of individual product categories was: American cheese, +1.6%; other cheese, +5.6%; nonfat dry milk, -2.3%; butter, +10.1%; and fluid milk, -1.4%.

U.S. dairy exports have been very strong in 2011 with fiscal year 2011(Oct-Aug) exports valued at $4.192 billion and a dairy trade surplus of $1.547 billion. Calendar year 2011 (Jan-Aug) exports were equivalent to 13.3% of total U.S. milk solids production, while imports were equivalent to only 2.8% (the lowest since 1996). August dairy exports equaled 14.4% of total U.S. milk solids production. In the first eight months of CY-2011 (Jan-Aug), exports accounted for 48% of NFDM/SMP produced by the U.S., 4.8% of the cheese, and 9.2% of the butter. However, August cheese exports were the lowest in nine months and off 10% as compared with August 2010.

Dairy Product Inventories: The latest USDA Cold Storage Report showed inventory decreases in September for American cheese (-1.1% at 632.6 million lbs.) and total cheese (-1.3% at 1,040.0 million lbs.) compared to September 2010. American cheese inventories set all-time monthly highs for each of the months from January through May, July and August. Total cheese inventory set monthly records for all months January through August. September butter inventory was 16.3% above September 2010, marking the second consecutive month butter inventory was above the same month in the previous year.

Outlook: Wholesale dairy product prices are mostly higher, but the U.S. dairy industry is also in the usual fall holiday sales season (Thanksgiving and Christmas). CME Class III futures prices are mixed with price averages expected to drop as we move into 2012. The 2011 CME Class III futures average is up (+$0.1841/cwt) at $18.09/cwt, while the price averages for the next 12 months and 2012 are down (-$0.0150/cwt and -$0.2575/cwt, respectively) to $16.87/cwt and $16.52/cwt, respectively. Milk production appears to have rebounded from the summer heat in most areas of the country with milk per cow in the U.S. up 1.1% in August and 0.7% in September versus August and September 2010. U.S. total milk production in September was up 1.7% which was only the second time since March that total milk production increased at or above trend (+1.6%). Dairy product commercial disappearance suffered greatly in May, June and July, down 1.4%, 3.2% and 0.2%, respectively, versus the same months in 2010 despite record dairy product exports. Consumer confidence has tanked since February and industry reports are indicating that the all-important fall dairy product sales season is not going as well as hoped for. If the fall holiday sales season is not robust look for cheese and butter prices to fall once wholesalers are satisfied enough dairy products have been purchased to cover anticipated Christmas season sales. This will undoubtedly translate into lower Class III and IV prices. I was hopeful that we would see cheese prices at least temporarily recover this fall to the mid $1.90’s. Now it appears that is very unlikely to happen. At this point it appears we will be lucky to maintain cheese prices in the mid to high $1.60’s for the remainder of the fall holiday sales season. Current cheese prices are only high enough to produce Class III prices in the neighborhood of $16.35/cwt. However, very strong dry whey prices (~$0.55/lb) are adding about another $1.00/cwt to the current Class III price. Dry whey futures are predicting at least a 14 cent drop by March. If this materializes Class III prices would fall about $0.84/cwt due to this factor alone. Producers should really consider forward pricing some milk soon.

Feed prices have moderated in recent weeks with corn and soybean meal prices down ~$1.40/bu and ~$50/ton over the past month. This presents a definite feed buying opportunity for dairy producers. It should also translate into healthier margins, but it may also decrease culling and increase milk per cow. Therefore, over the coming months I look for milk per cow to move back toward normal trend increases and for dairy cow numbers to once again steadily increase. Thus, look for dairy producer profit margins to really tighten as we move into 2012. Remember that past history has always shown that when margins become tighter U.S. dairy producers tend to increase milk production to meet cash flow needs. The U.S. dairy export market remains very strong, but there is much risk in the future outlook given all of the economic problems abroad and here at home. The economic crisis of 2009 showed how quickly export markets can decline. If U.S. dairy exports are negatively affected in any way over the coming months it could spell real trouble for farm-level milk prices. I advise dairy producers to keep a sharp eye on world economic developments and market milk into 2012 and 2013 accordingly.

To view a full report and other dairy marketing information go to my website at: www.msu.edu/~thomasc. This site also features a narrated Dairy Market Update powerpoint presentation. Both of these reports will be updated in early October. For assistance in calculating your cost of production, send me an email request (thomasc@anr.msu.edu).