Dairy Market Update, May 2013

Print

Print Email

EmailDairy market fundamentals are somewhat bearish in the near term but bullish in the longer term.

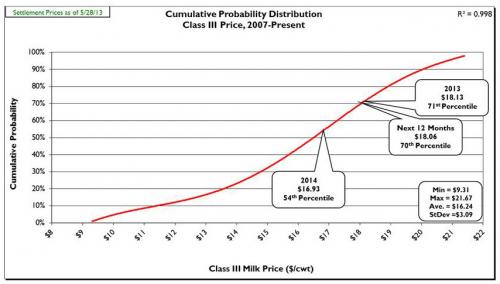

Prices: On Tuesday, May 28, 2013 spot prices for cheddar cheese blocks and barrels at the Chicago Mercantile Exchange (CME) were $1.7550/lb. and $1.7225/lb., respectively. CME block cheese prices are down since late April (4/29/13) -$0.1125/lb. and barrels are up +$0.0575/lb. During the same time period, butter is down to $1.5450/lb (-$0.1450lb.). The CME Class III futures averages (5/28/13) for 2013 were down to $18.13/cwt. (-$0.39/cwt.), the next 12-months was down to $18.06/cwt. (-$0.49/cwt.), and 2014 was up to $16.93/cwt. (+$0.07/cwt.). These Class III futures averages correspond to potential USDA Michigan mailbox prices of $19.14/cwt. (2013), $19.07/cwt. (next 12-months), and $17.94/cwt. (2014). Figure 1 shows the current (5/28/13) CME Class III futures averages for 2013, the next 12-months, and 2014 are at the 71st, 70th, and 54th percentiles, respectively.

Figure 1: Cumulative probability graph of USDA announced Class III prices (2007-present) and current CME Class III futures averages.

Supply: In April U.S. milk production rose 0.2 percent as compared with April 2012. This was obviously below trend increase (+1.5 percent, 2007-2011) and marked the tenth time in the past eleven months milk production grew below trend (+1.5 percent, 2007-2012). April production in Michigan increased 1.3 percent compared with April 2012. Due to “sequestration” budget cuts NASS did not report dairy cow numbers or milk per cow for April. However, dairy cow slaughter in April was up 28,600 head as compared to April 2012. Thus, it is probable the U.S. dairy herd shrank in April. Average cull cow prices have softened a bit, but remain historically high at $81.70/cwt. (-4.4 percent compared with April 2012). The USDA reports an increase in dairy feed prices in April of +3.8 percent compared with April 2012. The April milk:feed ratio, at 1.56, was below 2.00 for the 27th time in the past 29 months.

Demand: Total commercial disappearance of dairy products for 2012 finished the year slightly below trend (+1.5 percent, 2007-2012) at +1.4 percent. So far for CY-2013 (January-February) total commercial disappearance was up only 0.8 percent. February total commercial disappearance was a dismal -0.7 percent below February 2012. The January-February disappearance of individual dairy product categories was: American cheese, +1.8 percent; other cheese, +1.9 percent; nonfat dry milk, -18.7 percent; butter, +10.2 percent; and fluid milk, -3.3 percent (through March) as compared with February 2012.

U.S. dairy trade has shown trade surpluses for thirty seven consecutive months. March U.S. dairy exports were valued at $499.7 million, up 3.2 percent from March 2012. March marked the twenty fourth month out of the past twenty five in which exports exceeded $400 million, and equaled 13.5 percent of total U.S. milk solids production. For CY-2013 (January-March) U.S. dairy exports accounted for 41 percent of nonfat dry milk/skim milk powder produced in the U.S., 5.6 percent of cheese, 5.9 percent of butter; 46 percent of dry whey, and 72 percent of lactose.

Dairy Product Inventories: The latest USDA Cold Storage Report showed inventory increases in April for American cheese (+5.3 percent, 698.8 million pounds) and total cheese (+4.5 percent, 1,120.2 million pounds) as compared with April 2012. Both inventories were records for the month of April as well as all-time highs. April marked the fifth consecutive month total cheese inventory was above 1.0 billion pounds. April butter inventory was 22.2 percent above April 2012 at 310.7 million pounds, marking the twenty first consecutive month butter inventory was above the same month last year and setting an all-time record for butter inventory.

Outlook: Dairy market fundamentals continue on the bearish side, at least in the short run. Milk production is running basically even with last year; however, it should be remembered that U.S. milk production in Q-1 2012 was up 4.2 percent vs. 2011. NASS no longer reports cow numbers, at least for the remainder of FY-2013 (through September), therefore considering April dairy cow slaughter numbers were up 28,600 head as compared with April 2012 one would suspect the U.S. dairy herd shrunk a bit in April. Margins are obviously improving for dairy producers across the country so expect dairy producers to make a strong push to increase milk output in the coming months. Anecdotal reports support such a conclusion as both cheese plants and butter churns are running at, or near, full capacity across the country.

In the longer term many expect the U.S. dairy industry to contract, even in the face of healthy margins. Beef prices remain very strong and promise to strengthen further as steers are bringing in more dollars than dairy replacement heifers, and crossbred calves are more valuable than purebreds. Many are reporting sexed semen usage is down and some Holstein heifers have been sold at auctions in lots destined for the feedlot. Many believe this trend will continue pulling dairy animals to beef and eventually begin a noticeable shrinkage of the U.S. dairy herd.

Inventories of cheese and butter are at all-time historical highs and we are not finished with the spring flush (April-June). International dairy product prices, though high, have softened a bit recently. World demand for dairy products remains healthy and the USDEC estimates the top five dairy exporting regions (New Zealand, EU, U.S., Australia and Argentina) will be down over 1.0 percent in combined milk production for the first half of 2013 which is a shortfall of 1.6 million tons of milk vs. last year. Oceania has ended their 2012-2013 production season and reports stocks of finished products are only adequate for servicing existing accounts with little extra for other demand. A similar situation exists in the EU. Thus, U.S. dairy exports should remain strong as our domestic prices are below international prices. However, an increasingly strong U.S. dollar (+6.5 percent since February) may place some limits on U.S. dairy exports.

USDA measured feed prices were higher in April than last year (+3.8 percent as compared to April 2012). On the CME corn and soybean meal prices have recently shown some strength. Forage prices continue at historical highs as heat, drought, and reduced hay acreage played havoc with hay and corn silage production in 2012. The USDA reported the U.S. average alfalfa hay price was at $215/ton for April. Other reports indicate prime alfalfa in the Midwest has increased from $190/ton in April 2012 to $300 per ton in April 2013 (+58 percent) while prices have moderated a bit (-10.6 percent to $262/ton) in California’s Central Valley. Also, a recent USDA report showed nationwide alfalfa/alfalfa mixed hay production down 15 percent (Michigan was down 17.5 percent); the lowest production since 1953 and hay acreage is at the second lowest level on record. Further USDA reports indicate hay stocks are down about 34 percent vs. May 2012, with some states reporting declines of 50 percent or more (e.g., Mich., Minn., New York, Ohio, Vermont and Wisc.). Many of these declines are due to planting decisions and are unlikely to change the hay outlook very soon. There is also widespread concern in the upper Midwest of higher than normal winterkill for alfalfa this year which could dampen 2013 yields and cause further price increases and shortages. The current weather/planting situation should be monitored very closely and hay purchases made accordingly. Also, at this point in the season it appears the drought of 2012 will not extend into 2013, at least not in the major corn producing states.

The consumer confidence index rose to 76.2 in May, up from 61.9 in March and 69.0 in April and the highest in five years. However, it remains far short of the 90 level which is indicative of a healthy economy. U.S. dairy exports continue their strong pace, however, domestic total commercial disappearance of dairy products remains weak despite a seemingly stronger domestic economy. Some anecdotal reports are optimistic that food service orders for dairy products have shown some recent strength as Memorial Day signaled the beginning of the summer vacation season. However, it remains to be seen whether the 2013 summer vacation season will produce positive results for domestic dairy product consumption.

In the short term, I would not expect any significant strengthening of dairy prices until at least mid-July once the spring flush has waned and there is some indication of the summer vacation season spurring domestic dairy consumption. Strong international dairy prices, declining milk production in the five major dairy exporting nations and continued healthy international demand for dairy products should provide good support for higher U.S. milk prices as we move into summer and fall. As usual, summer weather will potentially impact the situation and deserves close monitoring. In the past, significant summer heat events are usually in place by mid to late June. So far that does not appear to be developing despite long range weather forecasts to the contrary. I expect much better milk pricing opportunities as we move into July and August as compared to current market conditions.

Michigan State University Extension recommends that producers sharpen their pencils, calculate their latest cost of production and formulate their 2013-14 milk and feed marketing plan. The market consistently shows it is impossible to sustain Class III prices in the +$20 range for any length of time as both domestic and export commercial disappearance are negatively affected. So, don’t let the “greed” stage of the “greed, hope and fear” cycle overly influence your pricing decisions. The USDA is forecasting record acreages of corn and soybeans for 2013 and a return to trend yields. Based on these assumptions, USDA economists are forecasting $4.80/bu corn and $10.50/bu soybeans for the 2013 crop. Feed prices at those levels would certainly fuel a surge in milk production here in the U.S. and likely around the globe. Keep your pencil sharp and don’t be afraid of pulling the trigger when prices are profitable even if continue to show strength. Selling into a strengthening market has always been a profitable strategy. Remember: marketing is first about price risk management and secondarily about profit enhancement. Work at increasing your overall average milk price rather than trying to hit the market high. To view a narrated PowerPoint based on this report go to www.msu.edu/~thomasc and click on the button “Narrated PowerPoint” on the front page (available 5/30/13 by 5 PM Eastern).

The latest USDA Milk Supply and Demand Estimates report for May saw forecasted 2013 milk production even at 201.8 B pounds (+0.7 percent vs. 2012) and forecasted fat basis commercial disappearance down slightly to 195.0 B pounds (+0.9 percent vs. 2012) despite “Exports are higher as abundant U.S. supplies and competitive prices are expected to spur foreign demand.” Forecasted 2013 wholesale dairy product and milk class prices were mostly higher in the USDA’s 2013 forecast for May.