Dairy Market Update, July 2011

Print

Print Email

EmailDairy market fundamentals and prices remain strong, but a great deal of risk remains in the market.

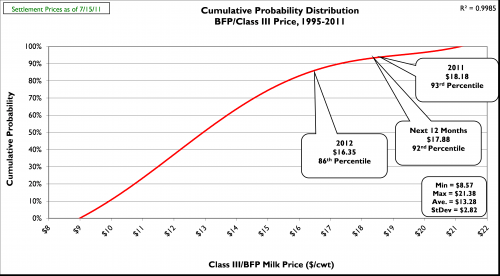

Prices: On Friday, July 15, 2011 spot prices for cheddar cheese blocks and barrels at the Chicago Mercantile Exchange (CME) were $2.0575/lb and $2.1100/lb, respectively. CME block cheese prices are down since mid-June (6/17/11) (-$0.0625/lb) while barrels are up (+$0.0425/lb). During the same time period, butter decreased (-$0.1100/lb) to $2.0300/lb. CME Class III futures averages for 2011, the next 12 months, and 2012 were $18.18/cwt, $17.88/cwt, and $16.35/cwt, respectively. These Class III futures averages correspond to potential USDA Michigan mailbox prices for 2011, the next 12 months, and 2012 of $19.17/cwt, $18.87/cwt, and $17.34/cwt, respectively. Figure 1 is a cumulative probability distribution of all USDA BFP/Class III monthly prices from 1995-present. The figure shows the current (7/15/11) CME Class III futures averages for 2011, the next 12 months, and 2012 are at the 93rd, 92nd, and 86th percentiles, respectively.

Figure 1: Cumulative probability graph of USDA announced monthly

BFP/Class III prices (1995-present) and current CME futures averages.

Supply: In May, U.S. milk production increased below trend (+1.6%, 1995-2011) at +1.3% compared to May 2010. May was the second consecutive month milk production grew below trend increase. May production in Michigan increased by only +0.3% compared to May 2010. The size of the U.S. dairy herd grew by 13,000 head from April to May, and is up 81,000 head versus May 2010. Dairy cow slaughter numbers in 2011 continue to run well ahead of last year, up 85,500 head compared to the same time frame last year (through 6/18/11). Average U.S. cull cow prices remained very high in June at $77.20/cwt (+33.3% compared to June 2010). Milk production per cow during January through May was slightly below trend increase. The USDA reported an increase in dairy feed prices in June of over 68.3% compared to June 2010; however, income over feed costs were up 19.9% (+$1.31/cwt) due to an increase of $5.60/cwt in the “All-milk” price.

Demand: The USDA reports total commercial disappearance in 2010 increased 3.3% over 2009, well-above the 1995-2009 average increase (+1.6%). All categories of wholesale dairy products showed above trend increases in disappearance for 2010 except fluid milk products. Total commercial disappearance remains strong in 2011, up 3.0% through April. All-time monthly records were set for January, February, March and April.those months. Through April, disappearance of individual product categories was: American cheese, +4.2%; other cheese, +7.1%; nonfat dry milk, -6.1%; butter, +15.3%; and fluid milk, -1.3%.

U.S. dairy exports for 2010 totaled $3.71 billion in value, up 63% from 2009. U.S. dairy imports in 2010 were the lowest since 1997. U.S. dairy exports continue strong in 2011 with January, February, March and April totaling $335 million, $348 million, $421 million and $403 million; +49%, +55%, +42% and +40% compared to January, February, March and April 2010. January through April 2011 exports were equivalent to 13.2% of total U.S. milk solids production; while imports were equivalent to only 2.8% (very near record lows). Cheese exports hit a record high in March at 49.3 M lbs., up 67% from March 2010 and equivalent to 5.4% of total U.S. cheese production for the month. So far in FY-2011 (Oct-Apr) U.S. dairy exports are valued at $2.517 billion (+46% versus FY-2010) with a dairy trade surplus of $820 million.

Dairy Product Inventories: The latest USDA Cold Storage Report showed inventory increases in May for American cheese (+0.9% at 620.5 million lbs.) and total cheese (+2.1% at 1,048.5 million lbs.) compared to May 2010. Both cheese inventories set all-time May highs, but are the lowest increase versus the same month last year since May 2008 (American cheese) and Nov 2008 (total cheese). May butter inventory was 19.8% below May 2010, marking the seventeenth consecutive month butter inventory has been below the same month in the previous year. Butter inventory declined March to April for the first time since 2004.

Outlook: Wholesale dairy product prices are mixed; however, they all remain above historical averages for this time of year. CME Class III futures prices are mixed; with close up prices up sharply. The 2011 and next 12 months average prices are up (+$0.4750/cwt and +$0.1967/cwt, respectively) while the 2012 average is down (-$0.1400/cwt). The spring flush of milk production is over and we are into the summer production season with its usual decline in both milk volume and milk components. Declining milk components means it takes a greater volume of milk to produce manufactured products (e.g., cheese and butter); but this is counter balanced somewhat as schools are closed for the summer break decreasing fluid milk needs and releasing more milk to manufacturing plants. In late summer and early fall wholesalers, in earnest, begin building cheese and butter inventories for the fall/winter holiday sales season. Even though feed prices are higher, margins for dairy producers are improving over last year (June income over feed cost +$1.13/cwt versus June 2010). High feed costs, high cull cow prices, and relatively low replacement cow prices should keep growth in milk per cow below trend rate for most of 2011. These factors should keep national milk production from getting ahead of commercial disappearance. World prices for dairy products have been weakening, however, U.S. dairy products at current prices remain competitive in the export market. Oceania reports no uncommitted stocks of manufactured dairy products, but the EU has some surplus products available for the spot export market. Domestically U.S. dairy market demand is sluggish. Consumer confidence is low, gasoline prices and unemployment are high, restaurant traffic has slackened, and mozzarella demand is slow. All of these factors point to a weak start to the summer travel season which means domestic demand for dairy products will suffer. In order to maintain the current strength in dairy product prices and milk prices it is critical to maintain our strong export market.

If the U.S. dairy export market retains its current strength, dairy producers will be rewarded with milk prices above historical averages. The current CME Class III futures average ($18.18/cwt) for 2011 is at the 93rd percentile of historical Class III prices (1995-present). This means that only about 7% of the monthly actual Class III prices since 1995 have been higher than $18.18/cwt. Although a crash in Class III prices is not anticipated, there remains a great deal of risk in the market. This is evidenced by the erosion of 2012 Class III futures prices. Most of this risk is on the demand side. Recent history has shown us that world events, whether natural disasters, political upheavals, or economic shocks, can have dramatic negative effects on commodity markets. With this in mind, dairy producers should give serious consideration to using price risk management tools (e.g., futures contracts, forward contracts, put options) to market some of their remaining 2011 milk production and reduce their milk price risk exposure. Feed prices continue to moderate, but the verdict is still out on the 2011 crop. Given the recent declines in corn, soybean, and hay prices dairy producers should consider forward pricing feed into the last half of 2011 and the first quarter or 2012. Dairy producers should remember that milk marketing is about price risk management first; profit enhancement is only a secondary consideration. For a full report and other dairy marketing information go to my website at: http://www.msu.edu/~thomasc. This site also features a narrated Dairy Market Update powerpoint presentation. For assistance in calculating your cost of production send me an e-mail request.